SUMMARY

At the 21st Conference of Parties (COP) in Paris in 2015, the member countries conveyed their efforts on climate change mitigation and adaptation commitments in their Nationally Determined Contributions (NDCs). Some South Asian countries such as Afghanistan, Bangladesh, Bhutan, India, Nepal, and Pakistan have considered using market mechanisms under Article 6 of the Paris Agreement to achieve their NDCs. These market mechanisms also gained a footing at the COP28 in Dubai in November-December 2023. Further negotiations on it have been postponed until the COP29 meeting in 2024 in Baku, Azerbaijan.

The commentary originally appeared in the Insights section of the Institute of South Asian Studies (ISAS), National University of Singapore (NUS). Read the original piece here.

Introduction

South Asia grapples with the impacts of climate change, given its geographical, environmental and developmental characteristics.[1] It is also the most densely populated region with developing economies, making it hard for governments to address climate change impacts independently. All the South Asian countries have signed the 2015 Paris Climate Agreement, a legally binding international climate change treaty that aims to limit global warming to below two degrees Celsius.[2] Countries have submitted their Nationally Determined Contributions (NDCs) under the United Nations Framework Convention on Climate Change (UNFCCC),[3] where they have outlined their climate action plans, strategies, and targets to mitigate greenhouse gas (GHG) emissions and adapt to the impacts of climate change.

To achieve the NDCs, the Paris Agreement lays out approaches for mitigation actions, adaptation planning, financial support, technology transfer, capacity building, loss and damage, and market and non-market approaches. Among these approaches, this paper examines the utilisation of market mechanisms under Article 6 of the agreement, particularly Article 6.4, which lays the foundation for countries to cooperate voluntarily to mitigate GHG through carbon emission trading. In this mechanism, an organisation operating in one nation can cut emissions within its borders and receive credits for those reductions. These credits can then be sold to another organisation in a different country, and the receiving company may utilise these credits to meet its emission reduction requirements or contribute towards achieving its net-zero goals. Six South Asian countries – Afghanistan, Bangladesh, Bhutan, India, Nepal and Pakistan – have indicated their intent to use market mechanisms in the NDCs.

This paper also assesses the readiness and implementation status of market mechanisms by six South Asian countries in achieving their NDCs. It contends that although market mechanisms show potential for addressing climate change in the region, substantial challenges must be tackled. The recommendations outline strategic approaches for governments and stakeholders to boost capacity and overcome barriers, facilitating the region’s effective implementation of market-driven climate actions.

Landscape of Market Mechanism Utilisation in South Asia

Market mechanisms provide financial incentives for cutting emissions, switching to low-carbon technology and encouraging environmentally friendly behaviours. The main mechanisms associated with carbon trading and their status in South Asia are detailed below.

Emission Trading System

The Emission Trading System (ETS), or cap-and-trade system, also called the compliance carbon market (CCM), is a regulatory system that binds companies operating within specified sectors to set their emissions below the allowable limit. Companies receive one unit of carbon permit for each metric ton of carbon dioxide or an equivalent GHG reduction, also known as allowances. Trading under the ETS can be done in both domestic and international markets. Only India has launched a domestic ETS in South Asia called the Carbon Credit Trading Scheme,[4] which it plans to operationalise in 2026.

India currently has the Perform, Achieve Trade scheme in place, which, is not a traditional ETS approach, but mandates companies in energy-intensive sectors to reduce their energy consumption and provides Energy Saving Certificates in exchange for energy savings that are traded at the power exchanges.[5] Pakistan has received support from the World Bank and the UNFCCC to establish a domestic ETS framework.[6] The country is currently working on the carbon market policy framework draft.[7]

Clean Development Mechanism

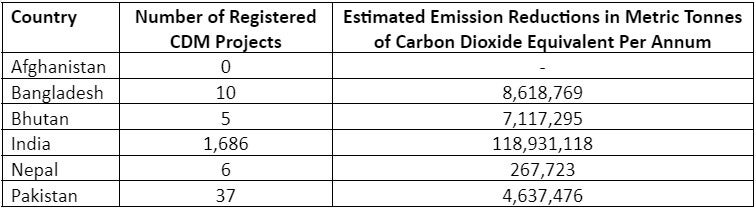

Most of the carbon market in South Asia operationalises in the form of a Clean Development Mechanism (CDM). Under the CDM, developed and industrialised countries that produce excess emissions invest in developing countries for emission reduction projects. In return, they receive Certified Emission Reduction certificates. Afforestation, energy efficiency, renewable energy and waste management projects are considered under the CDM. India is among the largest recipients of CDM projects in South Asia and globally.

Table 1: Number of Registered CDM Projects in South Asia

Source: CDM Registry,[8] November 2023

Joint Implementation

Joint Implementation enables a country (referred to as an Annex B Party)[9] that has agreed to reduce its GHG emissions to earn emission reduction units (ERUs) by tying up with another Annex B Party country.[10] These ERUs can contribute toward fulfilling the emission reduction targets outlined in the Kyoto Protocol. As of now, no South Asian country is an Annex B Party; hence, the region has not implemented this mechanism.

Voluntary Carbon Market

Voluntary carbon markets (VCM) operate independently of CCM, and the participation is voluntary. Participants engage in projects that reduce or capture GHG emissions and generate carbon offsets traded in the VCM. India is one of the biggest global players in the VCM. From 2010 to 2022, India represented 17 per cent of the worldwide supply to the VCM.[11] In December 2023, India announced the formation of a domestic carbon offset market where participants can register their projects as per the published sectoral methodologies.[12] While India is preparing to integrate with the global VCM market, Bhutan launched the National Carbon Registry in December 2023 that leverages a common data model with the Climate Action Data Trust (CAD Trust) meta-data layer capable of facilitating the transfer of unit ownership and identifying the status of carbon units, including issuance and cancellation status.[13] Bhutan is the first country in the world to integrate with the CAD Trust.

Regarding Pakistan, besides drafting the carbon market policy framework that is aimed to cover both CCM and VCM,[14] the country is working with the Verra Certification standard to increase the technical and administrative knowledge among stakeholders.[15] For Nepal, the largest project under carbon offsetting is the Forest Carbon Partnership Facility under the Reducing Emissions through Deforestation and Degradation programme, enabling the country to access up to US$45 million (S$60.45 million).[16] However, national efforts to promote the VCM domestically are lacking in Nepal, as well as in Afghanistan and Bangladesh, where VCM promotion at the national level is virtually non-existent.

Issues Affecting the Pace of Adoption of Market Instruments

Adopting market mechanisms in South Asia holds immense promise for advancing the efforts to achieve climate change goals. Yet, the region is slow to embrace the market mechanisms to fulfill its climate goals. The following are common issues hindering progress across the region:

- Inadequate Policy and Regulatory Framework: Most South Asian countries have charted their climate change policy. However, formulation of targeted policies and regulatory frameworks on carbon pricing mechanisms, cross-border emission trading, permitting procedures, and consistencies across sectoral policies for emissions undermines compliance and confuses entities striving to adhere to the targets while enabling others to circumvent government-set climate targets.

- Political Will and Governance: Policy implementation delays due to institutional reasons are common problems in most regional countries. Loose oversight also undermines the credibility of market mechanisms designed to incentivise emission reductions and can lead to suboptimal environmental outcomes.

- Access to Capital: To implement market instruments, a nuanced understanding of carbon markets, the financial tools, the market mechanisms and the frameworks that govern the carbon market is crucial. Since most South Asian countries are still developing, they rely on external agencies, resources, and expertise to navigate the complexities associated with market mechanisms. Similarly, transitioning to clean technologies requires substantial investments. Despite the potential of climate finance to support developing countries in using market mechanisms, the South Asian region has only received US$59.3 billion (S$79.66 billion) out of the US$446.98 billion (S$600.44 billion) allocated globally by multilateral banks and less than 10 per cent of project funding from the Green Climate Fund since 2011.[17]

- Lack of Regional Cooperation: South Asian resources and climate change impacts are transboundary. Limited initiatives for adopting market mechanisms on both bilateral and regional levels hinder the effectiveness of climate actions, especially in addressing transboundary issues that impact multiple countries in the region.

- Technology and Capacity Gaps: Market-driven climate solutions often require deploying specialised technologies, knowledge, and infrastructure. Lack of access to advanced monitoring technologies and expertise undermines the region’s integrity of emissions data, affecting the credibility of market-based approaches. Similarly, building and maintaining climate information systems, including satellite monitoring, IoT-based monitoring, and weather forecasting technologies, require significant resources and expertise, a major constraint for South Asian countries.

- Public Awareness and Stakeholder Engagement: Limited understanding among stakeholders on the impacts of climate change and the potential benefits of market tools to tackle the impacts of climate change are key obstacles in South Asia. This lack of awareness among the general public, businesses and communities leads to scepticism and resistance, posing challenges in establishing effective carbon trading systems. Additionally, insufficient knowledge of green finance discourages investment in sustainable projects, further complicating the implementation of climate-smart technologies.

Globally, adopting market mechanisms to achieve climate goals has been challenging. The COP28 Summit, held in December 2023, failed to agree on operationalising Article 6 of the Paris Climate Agreement. While the United States advocated for lax rules on the carbon market, which would allow the private sector to play a more vital role, the European Union voiced stricter guidelines that would hold parties accountable. Thus, the discussions have been pushed by a year until COP29.

Recommendations to Propel Market-driven Climate Action in South Asia

Strengthening Legal Framework for Effective Climate Action Implementation: To achieve climate goals through market approaches, governments must integrate climate strategies, enforce laws supporting climate actions, and regularly update legal frameworks to align with evolving priorities. This involves formulating and implementing legislation on emissions reduction targets, renewable energy development, penalties for environmental violations, and incentivising sustainable projects to catalyse climate innovation. These measures enhance the responsiveness and relevance of the legal framework to current and future climate goals.

Advocating and Coalition Building for Climate Prioritisation and Governance Strengthening: Engaging in advocacy campaigns at the political level, forming alliances with climate-conscious leaders, businesses, and civil society, and investing in enhancing institutions responsible for climate governance is crucial for prioritising and advancing the climate change agenda. This enhances the capacity of government agencies, environmental ministries, and regulatory bodies to design, implement, and monitor effective climate policies.

Formulating Strategic Financial Approaches for Climate Project Investment: Engaging international climate funds and financial institutions is crucial for investing in sustainable projects. Establishing transparent mechanisms for allocating and utilising climate finance, publishing progress reports, and implementing independent auditing reduces corruption risks and improves access to climate finance. Nationally, encouraging green bond issuance, providing financial incentives for private sector investments, exploring various financing models and using risk mitigation instruments address uncertainties and support climate goals.

Fostering Regional Collaboration for Climate Resilience: South Asian countries can initiate and strengthen bilateral and multilateral agreements and develop cross-border policies and frameworks that promote mutual support, information sharing, and joint initiatives on climate-related issues. A regional climate fund can be established to support collaborative projects addressing shared climate challenges, such as transboundary water management, biodiversity conservation, and disaster resilience. Additionally, shared systems can be developed to exchange information, research, and monitoring.

Promoting Sustainable Technology Adoption and Innovation in Climate Action: South Asian countries can identify key sectors where technology transfer is critical for climate action and establish mechanisms to exchange knowledge and expertise by formulating comprehensive national strategies and roadmaps. Similarly, establishing dedicated funds to support sustainable projects will incentivise innovation. Incentives such as tax credits, subsidies and recognition programs for entities adopting sustainable practices foster the adoption of climate-friendly technologies. Governments can also design frameworks that incentivise private sector involvement in technology transfer and implementation, fostering collaboration for sustainable development, which will help with the capital needs for implementing sustainable projects. Other initiatives that can boost the implementation of climate-friendly technologies are setting up technology incubators and innovation hubs that focus on climate-related solutions, investing in education and training programs to build a skilled workforce capable of implementing and managing climate-friendly technologies and investing in research and development initiatives that address climate challenges specific to South Asian countries.

Building Capacity through Strategic Climate Communication and Governance: Effective communication is vital for building stakeholder capacities in climate action. Governments should develop clear national communication strategies, emphasising the importance of market-driven climate actions and articulating their benefits to communities, the economy, and the environment. Implementing capacity-building programs for decision-makers on climate science, policies, and governance ensures informed decision-making. Additionally, fostering public participation and engaging civil society organisations enhance accountability and transparency in climate governance.

Conclusion

South Asia faces challenges, including inadequate policies, governance issues and limited resources, hindering the effective adoption of market-driven climate actions. Addressing these hurdles through legal frameworks, advocacy, financial approaches, regional collaboration, technology adoption and capacity-building is crucial for propelling the region towards sustainability and resilience. Strategic and concerted efforts are necessary to transform challenges into opportunities, fostering a collective commitment to environmental stewardship and climate action amid the adverse impacts of climate change.

About the Contributors

Ms Samridhi Pant is a Senior Researcher and Program Manager at the Nepal Institute for Policy Research, an independent and non-partisan research institute based in Kathmandu, Nepal. She can be contacted at [email protected].

Dr Amit Ranjan is a Research Fellow at the Institute of South Asian Studies (ISAS), an autonomous research institute at the National University of Singapore (NUS). He can be contacted at [email protected]. The authors bear full responsibility for the facts cited and opinions expressed in this paper.

References

[1] O P Mishra, “Seismic Microzonation Study of South Asian Cities and its Implications to Urban Risk Resiliency under Climate Change Scenario”, International Journal of Geosciences, Vol. 11 No. 4, April 2020, https://www.scirp.org/journal/paperinformation?paperid=99819; and Ravindra Kumar Srivastava, “Risk Profiles of South Asia-Urbanization Context”, Managing Urbanization, Climate Change and Disasters in South Asia, Disaster Studies and Management, Springer, Singapore, https://link.springer.com/chapter/10.1007/978-981-15-2410-3_1.

[2] “The Paris Agreement”, United Nations Framework Convention on Climate Change, https://www.un.org/en/climatechange/paris-agreement.

[3] “Nationally Determined Contributions”, United Nations Framework Convention on Climate Change, https://unfccc.int/process-and-meetings/the-paris-agreement/nationally-determined-contributions-ndcs.

[4] “Carbon Credit Trading Scheme, 2023”, Ministry of Power, India, 28 June 2023, https://powermin.gov.in/sites/default/files/uploads/4_Draft_notification_on_Carbon_Credit_Trading_Scheme_CCTS_regarding.pdf.

[5] “Status of Implementation of National Mission for Enhanced Energy Efficiency (NMEEE)”, PIB Delhi, Ministry of Power, Government of India, 29 March 2022, https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1811051.

[6] “Pakistan”, International Carbon Action Partnership, https://icapcarbonaction.com/system/files/ets_pdfs/icap-etsmap-factsheet-111.pdf.

[7] Fawad Yousafzai, “Govt all set to present draft Carbon Market Policy framework before federal cabinet for approval”, The Nation, 9 November 2023, https://www.nation.com.pk/09-Nov-2023/govt-all-set-to-present-draft-carbon-market-policy-framework-before-federal-cabinet-for-approval.

[8] As per the CDM registry available at https://cdm.unfccc.int/Registry/index.html.

[9] Kyoto Protocol to the United Nations Framework Convention on Climate Change, United Nations Framework Convention on Climate Change, 10 December 1997, https://unfccc.int/sites/default/files/resource/docs/cop3/l07a01.pdf#page=24.

[10] Ibid.

[11] “India’s national carbon market to seek links with international registries”, S&P Global Commodity Insights, 30 June 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/energy-transition/063023-indias-national-carbon-market-to-seek-links-with-international-registries#:~:text=India%20is%20one%20of%20the,by%20S%26P%20Global%20Commodity%20Insights.

[12] “India announces domestic voluntary carbon market scheme” S&P Global Commodity Insights, 20 December 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/energy-transition/122023-india-announces-domestic-voluntary-carbon-market-scheme.

[13] “Bhutan develops a high-integrity carbon market registry”, Kuensel, 5 December 2023, https://kuenselonline.com/bhutan-develops-a-high-integrity-carbon-market-registry/

[14] “Pakistan”, International Carbon Action Partnership, https://icapcarbonaction.com/system/files/ets_pdfs/icap-etsmap-factsheet-111.pdf.

[15] “Verra and Pakistan to Educate Carbon Market Stakeholders on Practical Insights, Technical Requirements, and Key Methodologies”, Verra, 29 June 2023, https://verra.org/verra-and-pakistan-to-educate-carbon-market-stakeholders-on-practical-insights-technical-requirements-and-key-methodologies/.

[16] “Everything you need to know about Nepal’s carbon trade deal”, The Kathmandu Post, 27 February 2021, https://tkpo.st/3pZMRHk.

[17] Masud M A K, Sahara J and Kabir M H, “A Relationship between Climate Finance and Climate Risk: Evidence from the South Asian Region”, Climate 2023; 11(6):119, https://doi.org/10.3390/cli11060119.